Editor: Readers, Oxbridgers can never be wrong! Zanny Minton Beddoes in even more toxic than Adrian Wooldridge & John Micklethwait of utterly notoriou’The Right Nation: Conservative Power in America’

Jul 05, 2026

Is The Economist always wrong?

We used artificial intelligence to test the accuracy of our forecasts

Jul 2nd 2026

https://www.economist.com/interactive/finance-and-economics/2026/07/02/is-the-economist-always-wrong

The tone of pronouncements made in the leader pages of The Economist has been likened to the “voice of God”. The comparison is not meant flatteringly. But it raises a fair question. A deity would be omniscient. How accurate, by comparison, are our predictions? Rigorous fact-checking usually saves us from embarrassing errors about the present. The future is trickier.

In 1999 we said oil could fall to $5 a barrel, from around $10 at the time. That $10 turned out to be a generational low. Prices rose more than tenfold in the next decade. Then, in 2013, we called a peak in global oil demand. Today it is still stubbornly trundling upwards. This April we said that oil markets were in “La La land” about the war in Iran and predicted a spike in prices. They have since fallen by about a third.

Perhaps the black stuff is our bête noire. Yet these howlers, and others, have given rise to the charge that, far from being all-knowing, The Economist is so reliably wrong that the smart move is to bet against it. There is no better time to double down on a stock-market rally than when we start fretting about a bubble. Last year the then chairman of Reform UK, a populist-right party, called The Economist the “ultimate contrarian indicator”, while complaining about our criticism of his party’s fantasyland fiscal numbers. (A few months later, the party reversed course and ditched those policies.)

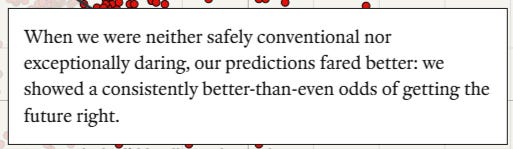

Is the accusation fair? Or can The Economist lay claim to a creditable forecasting record? Predictive perfection is not our goal and we aim mainly to inform and stretch minds. But ideally we would be right more often than wrong. To assess our record with something approaching neutrality, we took the 7,000 or so leaders The Economist has published this millennium and fed them into GPT-5.5, an artificial-intelligence model.

We asked it to assess whether each leader had made a falsifiable claim about the future as part of its main thesis. About 1,400 did. We then extracted those predictions, and asked the AI to mark out of ten both how contrarian the leader’s outlook was at the time and how accurate the prediction turned out to be. We ran those queries several times and took an average.

Overall, the AI assessor’s conclusions are reassuring, at least for those of us who make a living writing (and occasionally predicting) for The Economist.

Reader note the use of again the free-floating signifier as in revised July 2, 2026?

Editor: Reader recall my long comment on the use of The Economists ‘free floating signifier’ that appears and diapears, as an itegral part of the disengenious in another key?

Editor: Reader notice these five free floating paragraphs, as an itegral part to this exercise in self-serving prestidigitation, that represents a kind of bad faith, compleat with garish ilistrations, that appeares and dissapears. Not a surprise, as in carefullly revised July 2, 2026 essay!

…

Fuelled by war, colonisation and the industrial revolution, the British Empire overtook China as the world’s largest economy around 1840, when the first opium war between the countries was under way. America was, however, catching up fast.

The invention of the cotton gin in 1793 and brutal deployment of slave labour meant that the country produced most of the world’s cotton by the 1850s. America expanded, often violently, westward, gaining natural resources that would be the envy of the world.

…

Sprawling forests supplied timber for rapid construction. Well-positioned ports and the sweeping Mississippi river provided routes for export. Coal mines in Pennsylvania, Appalachia and the Midwest powered railroads and factories; the Great Lakes’ rich deposits of iron ore fed steel mills. Civil war ravaged the country but did not destroy it, ending slavery in 1865.

Industrialising rapidly, America overtook Great Britain as a guzzler of energy in 1891. We calculate that in 1899—after the Spanish-American war and the Treaty of Paris, which gave it control of Puerto Rico, Guam and the Philippines—it controlled more fertile land than any country bar the Russian empire. A few years later, in 1903, America had the world’s largest economy.

…

Sprawling forests supplied timber for rapid construction. Well-positioned ports and the sweeping Mississippi river provided routes for export. Coal mines in Pennsylvania, Appalachia and the Midwest powered railroads and factories; the Great Lakes’ rich deposits of iron ore fed steel mills. Civil war ravaged the country but did not destroy it, ending slavery in 1865.

Industrialising rapidly, America overtook Great Britain as a guzzler of energy in 1891. We calculate that in 1899—after the Spanish-American war and the Treaty of Paris, which gave it control of Puerto Rico, Guam and the Philippines—it controlled more fertile land than any country bar the Russian empire. A few years later, in 1903, America had the world’s largest economy.

…

Add immigration, a reliable rule of law, ample capital and animal spirits, and America’s economy raced ahead, growing more in absolute terms between 1945 and 1999 than any other country. Its researchers developed the building blocks of modern life, including the transistor, the computer chip, the personal computer and the internet.

…

Editor: The final paragraphs of this ‘essay’ is marked by The Economist Self-affirming chatter. It being just the companion piece to the other July 2, 2026 essay, now festooned with garish illustartions.

If The Economist was downbeat about the world’s economic prospects, we were exuberant about technology. Sometimes this exuberance turned out to be justified. We declared smartphones the future of computing in 2002, said that something like streaming would devour DVDs in 2008, and cautioned in 2011 that a flood of Chinese-made cars would wash over the West. Still, our techno-optimism occasionally got ahead of itself. Distributed electric grids (boosted by The Economist in 2000), cheap bioethanol (2003), open standards for social media (2008) and augmented reality (2016) have yet to bring about the breakthroughs we prophesied.

And then there is politics. It is not easy to foretell the decisions of voters or, for that matter, mercurial autocrats. The Economist was convinced by the false claim that Saddam Hussein was hiding weapons of mass destruction, but was right in 2003 to doubt Vladimir Putin was a true democrat. We toyed with the idea that China’s Communist Party might give ground on democratic reforms. In America we correctly forecast that Ted Cruz would not win the 2016 election, but for the wrong reason: we thought that his combative antics would alienate moderates. In fact, Donald Trump offered an even more furious alternative and still bested Hillary Clinton.

When covid-19 began infecting the globe, we were ahead of the crowd. By late January 2020, long before governments started ordering shutdowns, we had sounded the alarm that the disease would spread worldwide. By the end of February, we said it would be a pandemic. Stock markets tumbled by a quarter in the following weeks. Once pandemic stimulus spending fuelled inflation in 2022, we expected a much sharper rise in interest rates than the Federal Reserve, or bond markets, were pricing in. That turned out to be correct; our next bet, that this tightening would lead to a recession, did not. The world economy achieved a “soft landing” as inflation fell mostly back to normal.

So much for the past. As for the future, we expect the rich world’s debt binge to end in an inflationary mess and for AI to cause seismic economic and political disruption. We think that the global population will peak decades sooner than official projections. How are these predictions looking? It is, mostly, “too early to say”, as Zhou Enlai, communist China’s first premier, is misquoted as remarking when asked to assess the impact of the French Revolution. Come back in another quarter of a century to see how we did.

…

If The Economist was downbeat about the world’s economic prospects, we were exuberant about technology. Sometimes this exuberance turned out to be justified. We declared smartphones the future of computing in 2002, said that something like streaming would devour DVDs in 2008, and cautioned in 2011 that a flood of Chinese-made cars would wash over the West. Still, our techno-optimism occasionally got ahead of itself. Distributed electric grids (boosted by The Economist in 2000), cheap bioethanol (2003), open standards for social media (2008) and augmented reality (2016) have yet to bring about the breakthroughs we prophesied.

And then there is politics. It is not easy to foretell the decisions of voters or, for that matter, mercurial autocrats. The Economist was convinced by the false claim that Saddam Hussein was hiding weapons of mass destruction, but was right in 2003 to doubt Vladimir Putin was a true democrat. We toyed with the idea that China’s Communist Party might give ground on democratic reforms. In America we correctly forecast that Ted Cruz would not win the 2016 election, but for the wrong reason: we thought that his combative antics would alienate moderates. In fact, Donald Trump offered an even more furious alternative and still bested Hillary Clinton.

When covid-19 began infecting the globe, we were ahead of the crowd. By late January 2020, long before governments started ordering shutdowns, we had sounded the alarm that the disease would spread worldwide. By the end of February, we said it would be a pandemic. Stock markets tumbled by a quarter in the following weeks. Once pandemic stimulus spending fuelled inflation in 2022, we expected a much sharper rise in interest rates than the Federal Reserve, or bond markets, were pricing in. That turned out to be correct; our next bet, that this tightening would lead to a recession, did not. The world economy achieved a “soft landing” as inflation fell mostly back to normal.

So much for the past. As for the future, we expect the rich world’s debt binge to end in an inflationary mess and for AI to cause seismic economic and political disruption. We think that the global population will peak decades sooner than official projections. How are these predictions looking? It is, mostly, “too early to say”, as Zhou Enlai, communist China’s first premier, is misquoted as remarking when asked to assess the impact of the French Revolution. Come back in another quarter of a century to see how we did.

https://www.economist.com/interactive/finance-and-economics/2026/07/02/is-the-economist-always-wrong